arbitrage bellman ford|Crypto : Cebu Bellman-Ford Runtime What is the runtime of Bellman-Ford? Each edge is updated each iteration, with jVj 1 iterations. O(jVjjEj) Recall that in a dense graph with n vertices, . Sledujte Pinay tiktoker nag finger viral v Czech na Pornhub.com, nejlepší hardcore pornostránce. Pornhub je domovem té nejširší selekci Porna v Czech

PH0 · 图论正式发布!

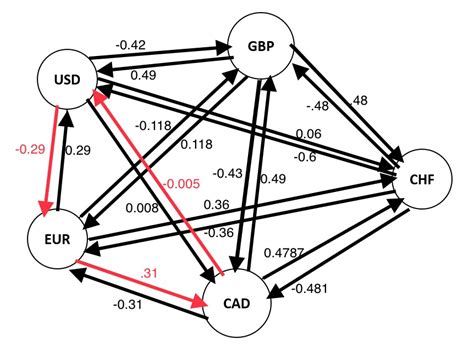

PH1 · Prajwal01221/Forex

PH2 · Mastering the Bellman

PH3 · Lecture 17

PH4 · Crypto

PH5 · Bellman Ford currency arbitrage detection algorithm

PH6 · Arbitrage with the Bellman

PH7 · Arbitrage using Bellman

PH8 · Arbitrage opportunity in python with bellman

PH9 · 1.Bellman

Elemento Ng Tula - Download as a PDF or view online for free. Submit Search Submit Search. Upload. Elemento Ng Tula . SUKAT Ito ay tumutukoy sa bilang ng pantig ng bawat taludtod na bumubuo sa isang saknong. Ang pantig ay tumutukoy sa paraan ng pagbasa. halimbawa: isda – is da – ito ay may dalawang pantig is da ko sa .

arbitrage bellman ford*******代码随想录算法训练营第61天|Bellman_ford 队列优化算法(又名SPFA)、bellman_ford之判断负权回路、bellman_ford之单源有限最短路 这道题和上一题的区 . 以最短路算法为例,《算法4》,只讲解了 Dijkstra(堆优化)、SPFA (Bellman-Ford算法基于队列) 和 拓扑排序, 而 dijkstra朴素版、Bellman_ford 朴素版 .

Bellman-Ford Runtime What is the runtime of Bellman-Ford? Each edge is updated each iteration, with jVj 1 iterations. O(jVjjEj) Recall that in a dense graph with n vertices, .

Bellman-Ford algorithm: The Bellman-Ford algorithm finds the minimum weight path from a single source vertex to all other vertices on a weighted directed .

Now, all we need to do is apply the Bellman-Ford algorithm to detect a negative loop, which indicates an aribitrage opportunity. Why? Because a negative loop indicates you . In this project, we study the arbitrage problem and design classic algorithms for it. We have a fixed amount of assets, for example, US dollars. We are given a set of . Arbitrage Opportunities: On the flip side, in some financial scenarios, negative cycles represent arbitrage opportunities. Traders can exploit these cycles to .Application of the Bellman Ford (shortest-path) Algorithm to detect real time arbitrage opportunities in currency trading. - d-roizman/Bellman-Ford-currency-arbitrage

This project implements the Bellman-Ford algorithm to identify arbitrage opportunities in the foreign exchange (forex) market. The Bellman-Ford algorithm is adapted here to .

In this project, we study the arbitrage problem and design classic algorithms for it. We have a fixed amount of assets, for example, US dollars. We are given a set of currencies and a set of currency exchange rates. The objective is for a cycle, starting from US currency, and ending at US currency so that we can have more assets by .

Bellman-Ford Algorithm. Bellman-Ford is a single source shortest path algorithm that determines the shortest path between a given source vertex and every other vertex in a graph. This algorithm can be . In 2016, I started down a path that would consume me for the next few years—cryptocurrency arbitrage. A game where millions of dollars are at stake and mere milliseconds separate the winners from the losers. . As we need the shortest path in a graph with negative edge weights, the Bellman-Ford algorithm is the best choice. It is .

Tìm hiểu về thuật toán Bellman-Ford. Dẫn nhập. Trong bài học trước, chúng ta đã cùng nhau đi tìm hiểu về thuật toán Floyd-Warshall trong tìm kiếm đường đi ngắn nhất trên đồ thị.Bellman Ford's Algorithm is similar to Dijkstra's algorithm but it can work with graphs in which edges can have negative weights. In this tutorial, you will understand the working on Bellman Ford's Algorithm in Python, Java and C/C++. Courses Tutorials Examples . Try Programiz PRO.

The basic premise of arbitrage is to buy something for one price and instantly sell it for another. In our case, we want to find a currency with a price discrepancy, e.g. one where converting between multiple currencies will eventually lead you to make more money in your starting currency than you began with.

arbitrage bellman ford CryptoThe basic premise of arbitrage is to buy something for one price and instantly sell it for another. In our case, we want to find a currency with a price discrepancy, e.g. one where converting between multiple currencies will eventually lead you to make more money in your starting currency than you began with.Cryptoduring an arbitrage as an investor who enters the market early, makes the maximum profit. In our experiment, A Bellman-Ford based model is used for detecting the mis-pricing. Keywords:- Arbitrage; Bellman-Ford; foreign exchange; hedging. I. INTRODUCTION Arbitrage is the trading strategy which earns a risk-free profit.

Bellman-Ford algorithm: The Bellman-Ford algorithm finds the minimum weight path from a single source vertex to all other vertices on a weighted directed graph. Our goal is to develop a systematic method for detecting arbitrage opportunities by framing the problem in the language of graphs. Approach Bellman-Ford is an algorithm to find the shortest path between a source and a target, given X weight per edge. It does this by adding the weights of a path to get a total path weight.Pre-requisite: Bellman-Ford Algorithm & Negative Cycle Detection In the previous chapter while studying Bellman-Ford Algorithm we saw that in every iteration we are considering all the edges and trying to relax them. But, if we give it a little bit thought we would notice that in every iteration we would need to relax only those vertices for which at least one of .arbitrage bellman fordThis FX Arbitrage problem set involves using a shortest paths algorithm (Bellman Ford) to find arbitrage opportunities - potentially profitable currency trades in a given currency table. Resources. Readme Activity. Stars. 4 stars Watchers. 2 watching Forks. 0 forks Report repository Releases No releases published. poj-2240-Arbitrage(Bellman-ford算法练习 + Floyd算法练习) Masker_43 回复 #魔君#: 那如果源点 1 与其他点都不连通,不是直接退出了吗?题里没有保证环路必须经过第一种货币啊。 poj-2240-Arbitrage(Bellman-ford算法练习 + Floyd算法练习) Masker_43 回复 #魔君#: 对,感谢。Arbitrage is the process of using discrepancies in currency exchange values to earn profit. Consider a person who starts with some amount of currency X, goes through a series of exchanges and finally . That calls for the Bellman-Ford algorithm with the edge weights transformed such that the w' = -ln(w). The reason for that transformation is . An explanation of arbitrage and a look at an efficient algorithm to find riskless instantaneous arbitrage opportunities across markets. Read Write. . The Bellman-Ford Algorithm. The problem of finding shortest paths is a common and fundamental problem in computer science, which can be applied to many different .

forex arbitrage forex-trading bellman-ford-algorithm arbitrage-opportunity arbitrage-trading Updated Jan 8, 2018; Python; hlefebvr / shortest-path-gtfs Sponsor Star 7. Code Issues Pull requests Data exploitation for graph algorithms - applied to Paris. graphs gtfs dijkstra dijsktra .L'algoritmo di Bellman-Ford calcola i cammini minimi di un'unica sorgente su un grafo diretto pesato (dove alcuni pesi degli archi possono essere negativi). L'algoritmo di Dijkstra risolve lo stesso problema in un tempo computazionalmente inferiore, ma richiede che i pesi degli archi siano non-negativi. Per questo, Bellman-Ford è usato di solito quando sul . Source code for the HappyCoders.eu articles on pathfinding and shortest path algorithms (Dijkstra, A*, Bellman-Ford, Floyd-Warshall). . 📈💰Arbitrage Detector for the Foreign Exchange Market. trading graphs forex arbitrage bellman-ford . Using Bellman-Ford, find and return negative-weight cycles if they exist. Calculate the arbitrage that these negative-weight cycles correspond to. The full code for this project can be found in this GitHub repo.s. Star. Raw data. For the raw data, I decided to use the CryptoCompare API which has a load of free data compiled across multiple .

Discover the NCAAB odds and predictions covers contest players are making with consensus picks All Leagues NFL NCAAF MLB CFL WNBA Overall Team Money Leaders Top 10%

arbitrage bellman ford|Crypto